Step-by-Step Guide to Applying for a Bike Loan Online & Offline

Table of Contents

- • Introduction

- • Why Apply for a Bike Loan?

- • Eligibility Criteria for a Bike Loan

- • Documents Required

- • Applying for a Bike Loan Online

- • Applying for a Bike Loan Offline

- • Comparing Online vs. Offline Bike Loans

- • Tips to Get the Best Bike Loan Deal

- • FAQs

- • Conclusion

Introduction

Owning a bike is a dream for many, whether for convenience, adventure, or daily commuting. However, purchasing a bike outright may not be feasible for everyone. This is where a bike loan comes in. Whether applying online or offline, this step-by-step guide will help you understand the process efficiently.

Why Apply for a Bike Loan?

• Affordability : Spread the cost into manageable EMIs

• Minimal Documentation : Banks and NBFCs offer easy documentation processes.

• Flexible Repayment Tenure : Choose loan tenures from 12 to 60 months

• Competitive Interest Rates : Many lenders provide attractive rates, especially for salaried individuals.

Eligibility Criteria for a Bike Loan

To qualify for a bike loan, you must meet certain criteria:

• Age : 18 to 65 years (varies by lender).

• Employment : Salaried with a stable income.

• Income Requirement : Typically, INR 30,000 per month or more.

• Credit Score : A good score (550+) increases approval chances.

• Residence Stability : Proof of residence required, typically 1+ year at current address.

Documents Required

Before applying, keep these documents ready:

• Identity Proof : Aadhaar Card, PAN Card, Voter ID, or Passport.

• Address Proof : Utility bills, Aadhaar Card, or Rental Agreement.

• Income Proof : Salary slips (for salaried individuals) or ITR (for self-employed individuals).

• Bank Statements : Typically, last 3 to 6 months.

•Passport-sized Photographs

Applying for a Bike Loan Online

Applying online is convenient and quick. Follow these steps:

Step 1: Research and Compare Loan Offers

Visit various banks’ and NBFCs’ websites to compare interest rates, tenure, and EMI options.

Step 2: Check Your Eligibility

Use an online eligibility calculator to determine how much loan you can avail yourself of.

Step 3: Fill Out the Application Form

Most lenders provide a digital form where you need to enter your details such as name, income, and bike model.

Step 4: Upload Required Documents

Scan and upload KYC documents, income proof, and address proof

Step 5: Await Verification and Approval

Lenders verify your details and creditworthiness. Approval time can range from a few hours to a couple of days.

Step 6: Loan Disbursal & Bike Purchase

Once approved, the loan amount is either credited to your account or directly to the bike dealer.

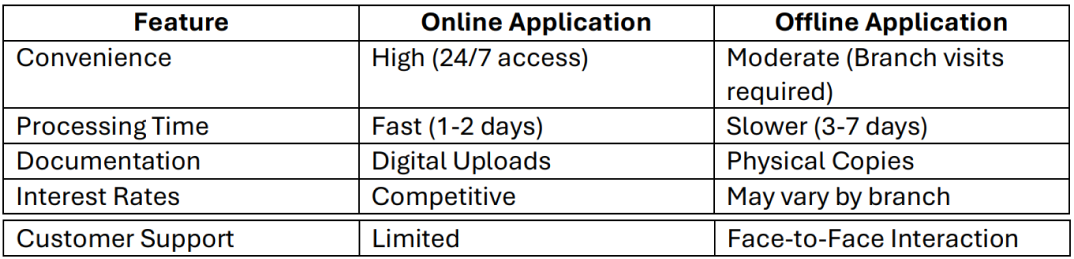

Comparing Online vs. Offline Bike Loans

Here is a list of some banks and the interest rates they offer:

Tips to Get the Best Bike Loan Deal

• Maintain a Good Credit Score : A higher score ensures lower interest rates.

• Compare Multiple Lenders : Always check for the best rates and terms.

• Negotiate Processing Fees : Some lenders may waive or reduce fees

• Opt for a Shorter Tenure : Lower interest cost overtime.

• Check Hidden Charges : Ensure there are no prepayment penalties or hidden fees.

Applying for a bike loan online or offline is a straightforward process when you follow the right steps. While online applications provide speed and convenience, offline applications allow direct interaction with bank representatives. Choose the method that suits you best, compare offers, and ride away with your dream bike hassle-free!

Frequently Asked Questions

Q1: Can I get 100% financing for my bike loan?

A: Yes, some lenders offer 100% financing, but eligibility depends on your credit score and income.

Q2: What is the typical interest rate for a bike loan?

A: Interest rates range between 7% to 15%, depending on the lender and your credit profile.

Q3: How long does it take to get a bike loan approved?

A: Online applications take 1-2 days, while offline applications may take 3-7 days.

Q4: Can I prepay my bike loan?

A: Yes, most lenders allow prepayment but check for prepayment charges.

Q5: What happens if I miss an EMI payment?

A: Missing an EMI can lower your credit score and result in penalty fees.

Share this post: