Middle-Class Financial Traps in India: Why Debt Keeps Rising and What to Do About It

For most Indian middle-class families, financial instability does not arrive as a single dramatic event. It builds quietly, one commitment at a time, until a month arrives where the salary is spent before it lands. India's household debt reached 42.9% of GDP in June 2024, roughly triple the absolute levels seen a decade earlier, according to the Times of India. What makes that number more striking is where the borrowing is going: RBI-linked data shows that non-housing retail loans now form 54.9% of household debt, per a Canara Bank analysis of the RBI Financial Stability Report. More households are borrowing to cover current consumption rather than to build an asset. That shift is the structural story behind a debt problem that has been growing for years.

Why Debt Is Rising: The Core Drivers

The pressure on middle-class household finances is not primarily a spending discipline problem, though that plays a role. It is a structural mismatch between the pace at which costs rise and the pace at which salaries do.

- Income Growth Lagging Costs: Over the past decade, middle-class income growth has broadly failed to keep pace with the rising cost of food, rent, healthcare, and education. The nominal salary number may look higher, but purchasing power has not kept up. What a household could manage on one income a decade ago frequently requires either two incomes or supplementary borrowing today.

- The Shift to Consumption Debt: When more than half of household debt is going toward current consumption rather than property or productive assets, it signals that borrowing is filling a gap in monthly income, not funding long-term growth. Debt that pays for groceries or utility bills this month still needs to be repaid next month, from the same salary that could not cover this month's costs.

- The Velocity Mismatch: Salary arrives once a month. Spending obligations, EMIs, rent, school fees, household costs, arrive continuously. Many urban households find a large share of take-home pay committed to fixed obligations in the first week or two, leaving a shrinking buffer for anything that follows. When an unexpected expense lands in week three, the only options are savings or borrowing.

- Aspirational Pressure: Social comparison has always existed. Platforms that make everyone else's lifestyle visible and immediate have accelerated it significantly. Borrowing to fund a holiday, a phone upgrade, or a vehicle that stretches the budget is not irrational behaviour from a social signalling perspective. It is, however, debt that rarely improves the underlying financial position.

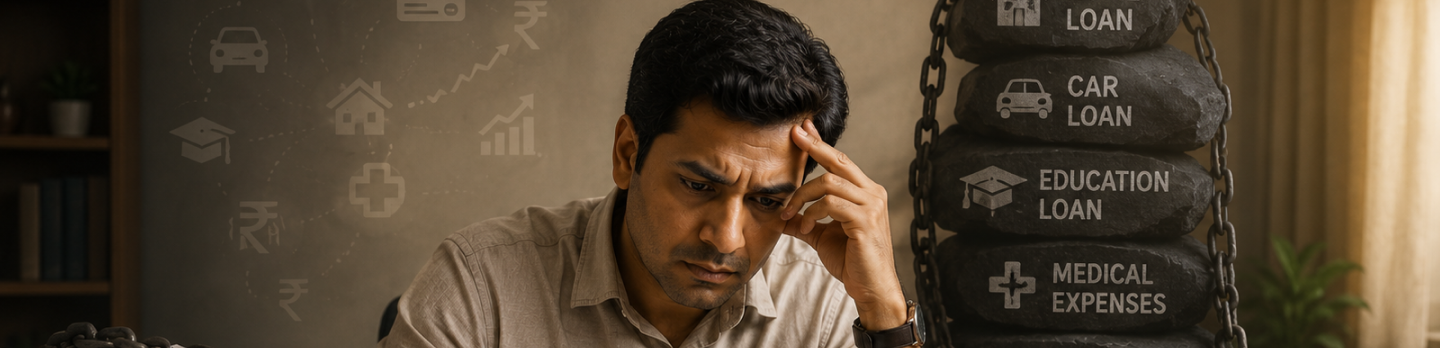

The Major Financial Traps

1. The Wedding Trap

Wedding expenses in India carry enormous social weight and, for many families, enormous financial consequence. The pressure to host an event proportionate to perceived social standing regularly leads to borrowing that persists well beyond the wedding itself, sometimes for years. Debt taken on for a single day's event competes with savings that should be going toward housing, health, and education. For a closer look at how short-term borrowing intersects with large one-off expenses, the use cases page covers the range of scenarios AFI's products address.

2. The Healthcare Shock Trap

India's private healthcare sector has advanced considerably. Its billing capacity has advanced with it. A serious hospitalisation, whether planned or sudden, can generate costs that overwhelm savings accumulated over years. Most Indian households remain significantly underinsured, which means medical emergencies convert quickly into borrowing events. The Medical Emergencies and Emergency Loan pages cover how AFI's products are structured for exactly this kind of unplanned, time-sensitive need.

3. The Education Debt Trap

Education borrowing in India, particularly for professional and post-graduate programmes, has grown significantly. The challenge is that the returns on that investment are uneven. When a degree does not translate into employment at the income level needed to service the loan, the borrower carries the debt forward while the salary trajectory disappoints. For families supporting children through higher education, the financial pressure compounds across two generations simultaneously.

Signs You Are in a Debt Trap

The markers are usually visible before the situation becomes critical, if you are looking for them:

- A large share of your monthly salary is committed to EMI payments before any discretionary spending begins.

- You are consistently paying only the minimum amount due on credit card statements, which means the outstanding balance is compounding at a high interest rate.

- You have taken a new loan to close or manage an existing one. This practice delays the problem and increases its total cost.

- Loan applications are being rejected due to a low credit score or a debt-to-income ratio that lenders consider too high.

- Your emergency fund, if one exists, is being used to cover regular monthly expenses rather than genuine emergencies.

What to Do: A Strategic Recovery Plan

1. Adopt a Three-Account System

Separating money by purpose is a simple but effective way to make spending patterns visible. Keep a dedicated account for salary credit, a second for monthly household expenses, and a third for savings and investments. When the expense account runs low before the month ends, that is a signal to review spending, not a prompt to transfer from savings. The physical separation creates a natural checkpoint that a single account does not.

2. Prioritise Health Insurance

A single hospitalisation without adequate cover can set back years of savings progress. An IRDAI-regulated health insurance plan, sized appropriately for your household's actual medical risk, is not optional infrastructure. It is the most cost-effective way to prevent a healthcare event from becoming a debt event. For households that have borrowed to cover medical expenses in the past, reviewing cover adequacy is the first step in breaking that cycle. The Medical Emergencies page covers bridge borrowing for when insurance does not cover the full cost or the settlement is delayed.

3. Use Strategic Debt Repayment

- Snowball Method: Clear the smallest outstanding loan first, regardless of interest rate. The psychological momentum from closing an account completely is a real and documented factor in sustained repayment behaviour.

- Avalanche Method: Target the highest-interest obligation first, typically credit card debt. This minimises total interest paid over the repayment period and is the mathematically optimal approach for reducing total debt cost.

- Loan Restructuring: If monthly EMI obligations are creating consistent shortfalls, discuss tenure extension with your lender. A longer tenure reduces the monthly outflow, though it increases total interest paid. For borrowers managing multiple obligations simultaneously, the Debt Consolidation option is worth reviewing.

4. Choose Regulated Borrowing When You Need a Bridge

When a short-term cash need is genuine and bounded, the choice of lender matters as much as the decision to borrow. Unregulated quick-loan apps operating outside the RBI framework have been documented charging effective rates that compound a debt problem rather than solving it. Ayaan Finserve India (AFI) is an RBI-registered NBFC (Reg. No. B-14.01220) that operates under defined obligations on disclosure, data privacy, and recovery conduct.

- Transparency: Every AFI loan includes a Key Fact Statement disclosing the full APR, all charges, and the complete repayment schedule before the agreement is signed.

- Borrower Protection: AFI adheres to the 2026 RBI digital lending framework, including the cooling-off period provision. The 2026 RBI Personal Loan Guidelines article covers each borrower protection in plain language.

- Accessibility: AFI's Instant Personal Loan products support salaried professionals with CIBIL scores from 500 upward, for amounts up to ₹1 Lakh through the Dhanvriddhi range.

The goal is not to avoid borrowing entirely. It is to avoid debt that funds depreciating assets or covers structural income shortfalls without addressing the underlying gap. A short-term loan used as a genuine bridge, repaid within the agreed window, does not create a debt trap. A pattern of rolling short-term debt from one month to the next does. That distinction is worth keeping visible, particularly when the next cash crunch arrives and the fastest available option looks like the most convenient one.

Frequently Asked Questions (FAQs)

1. How do I know if I am in a debt trap?

The clearest signal is when a significant portion of monthly salary goes toward servicing existing debt before any living expenses are covered. Other markers include borrowing to repay existing loans, consistent credit card minimum-only payments, and declining applications from lenders due to high existing obligations.

2. What is the difference between good debt and bad debt?

Good debt is borrowing that builds or protects an asset: a home loan, an education loan for a programme with clear employment outcomes, a business loan that generates returns above its cost. Bad debt funds consumption, depreciating assets, or lifestyle expenses that leave nothing behind after the loan is repaid. The distinction is not always clean in practice, but it is the right frame for evaluating any borrowing decision.

3. Is debt consolidation a good idea?

It depends on the terms. Consolidating multiple high-interest obligations into a single lower-rate loan reduces total monthly outflow and simplifies repayment tracking. The risk is that borrowers who consolidate without changing the spending behaviour that created the original debt find themselves back in the same position within a year or two. Consolidation addresses the symptom; the budget restructure addresses the cause. The Debt Consolidation page covers how AFI's product is structured for this purpose.

4. How do I rebuild a credit score damaged by debt stress?

Consistent on-time repayments on active credit accounts are the primary mechanism. Small installment loans serviced correctly build positive bureau data relatively quickly under the 2026 reporting cycle, which updates more frequently than the previous monthly schedule. The credit score repair guide on this blog covers the specific strategies in detail.

5. When should I use a short-term loan during a financial crunch?

When the cash gap is specific, bounded, and temporary, a known expense before a salary that will cover the repayment. Not as a recurring mechanism to extend a monthly shortfall that the salary cannot resolve. The short-term lending page covers the 30-day structure and repayment options available through AFI.

Disclaimer: This article is intended for general informational purposes only and does not constitute legal, tax, or investment advice. Financial regulations and individual circumstances vary. Readers are advised to consult a qualified financial or tax professional before making any borrowing or investment decisions.

Share this post: